Table of Contents

About the Author

More Posts

Again?! Already?! Didn’t we just pay our quarterly estimates?

If you’ve ever felt that, or said that out loud, then you’re in good company. Every small business owner has probably had the same thought at least a few times in their business journey.

Many seem to experience this on a quarterly basis.

It’s amusing because quarterly tax payments are one of the most predictable things in your business. You can literally circle the dates on your calendar. Yet we often find ourselves surprised and unprepared when those dates arrive.

In this world nothing can be said to be certain, except death and taxes.

There’s got to be some way of getting off the carousel, right?

You need a simple system

If you want your business to grow then you have to start putting simple and repeatable systems in place.

They need to be simple and repeatable because if they aren’t you won’t use them. And if they aren’t simple and repeatable, then you won’t eventually be able to delegate someone else to do the job for you.

You do not rise to the level of your goals. You fall to the level of your systems.

So, let’s talk about a simple system to make sure you always have enough money set aside to pay taxes.

Both Mike Michalowicz and Donald Miller talk about similar systems in greater detail in their books Profit First and How to Grow Your Small Business, but I’ll cover the basics here.

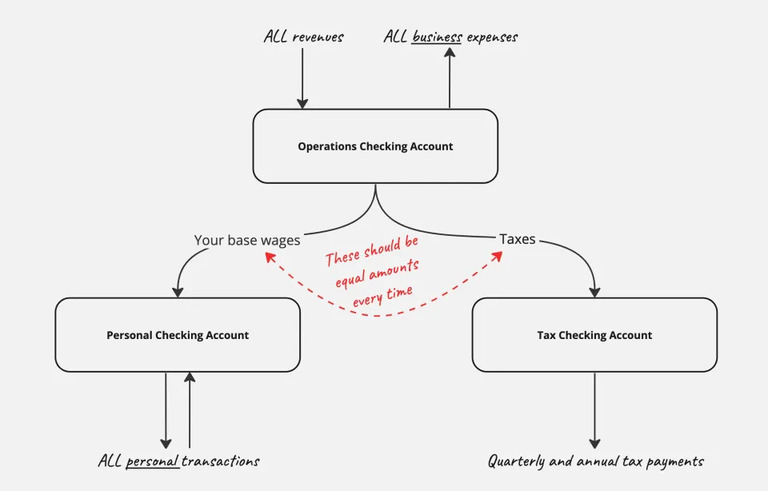

You need at least three separate checking accounts

- The operations account: all business-related transactions happen from this account.

- Never allow any personal expenses or other activity that isn’t related to the business.

- All revenues come into this account.

- All expenses (except for taxes) are paid from this account.

- Your personal account: the account you personally live from.

- Never make any business purchases from this account.

- The tax account: this is where you’ll set aside money to pay taxes.

How the system works

Here are the basics.

All business-related revenues and expenses flow in/out of the operations account.

When you pay yourself, you transfer your base wages from the operations account to your personal account. It’s up to you to determine how much you’re going to pay yourself, but I’d recommend that this be a reasonable living wage and no more. If you’re just getting started with your business, you may want to keep this very minimal in the beginning.

This is the most important piece - every single time you pay yourself, you also have to account for taxes. Remember, you pay taxes on your profits (when your revenues exceed your expenses). By definition, when you pay yourself wages, you are treating that money as profit. Note: don’t get confused by this. Paying yourself wages may look like an expense from the business’ perspective, but since you are the owner, the IRS views your wages as paying yourself the profits.

So, here’s the rule: every time you pay yourself, you must put an equal amount into the tax account.

For example: if you pay yourself $2,000 every two weeks, here’s what that should look like:

- Transfer $2,000 from the operations account to your personal account.

- Transfer $2,000 from the operations account to the tax account.

Isn’t that setting aside too much for taxes?

If you’re paying attention, that looks like you’re setting aside 50% of the business profits to account for taxes. That’s right!

In most cases, you will have too much money set aside at the end of the year. That’s actually what we’re aiming for, and here’s why:

- Depending on your state, the sum of your state income taxes and your federal income taxes is going to add up to somewhere close to the 50% threshold.

- If you’ve been running a profitable business for more than a few minutes, you know that estimating taxes throughout the year is as much art as it is science. You don’t want to end up with too little set aside for taxes, and then to be scrambling (again) to find the cash to pay the final tax bill.

- You’re likely to have some left over at the end of the year when the final tax bill is taken care of. Hooray! Bonus for you!

Now, I did say this was a very simple system. In my opinion, the best systems are the simplest ones, because those are the ones that you understand and the ones you’ll actually use.

There is definitely more to consider in building a cash management system, but this is a really good start that will leave you confidently prepared for taxes.

If you want some help implementing a better cash management system for your business, I teach a 1:1 cash management workshop. You’ll finish that workshop with a fully functional system for streamlining how you manage cash, along with a thorough understanding of how to use that simple system so that you always have enough to pay taxes and maximize your business profit. Give me a call if you’re interested.

To thriving,

- Zach